Are you holding company stock in your retirement plan?

If so, Net Unrealized Appreciation (NUA) could be your key to significant tax savings. This often-overlooked strategy allows you to potentially pay less in taxes on your employer stock when you retire, putting more money in your pocket when you need it most.

This guide will walk you through much of what you need to know about NUA: what it is, how it works, and most importantly, how to use it to optimize your retirement savings.

Whether you're years from retirement or actively planning your exit strategy, understanding NUA could make a substantial difference in your financial future.

If you want help understanding the best NUA strategy for your situation, talk to an experienced financial advisor by requesting a free personalized retirement assessment.

Table of Contents:

What is Net Unrealized Appreciation?

Net unrealized appreciation (NUA) is the increase in value of employer stock held in a tax-deferred retirement savings plan like a 401(k).

It represents the difference between the stock’s cost basis (what you originally paid) and its current market value.

For example, if you bought company stock at $20 per share through your 401(k), and now it’s worth $60, your NUA is $40 per share.

Grasping this “hidden” gain within your retirement savings is crucial for tax planning.

This allows investors to understand the advantages of appreciated employer stock.

Such appreciated employer stock allows investors to strategize according to the rules available for this asset class when thinking about different investment strategies and capital gains implications during wealth management decisions for federal taxes.

How NUA Works in Retirement Plans

When it comes to company stock in your 401(k), the IRS offers a special tax advantage through NUA that could save you thousands on taxes in retirement. While most 401(k) withdrawals are taxed as ordinary income (which could be as high as 37% in 2024), NUA allows you to pay potentially lower capital gains rates on a portion of your employer stock's value.

However, timing is crucial - this tax break only applies when you take a lump-sum distribution or rollover of your entire 401(k) balance at once.

Like all 401(k) investments, your company stock grows tax-deferred while it stays in your retirement account.

But here's where NUA offers a unique advantage: Instead of paying high ordinary income taxes on all your gains when you withdraw, you can potentially pay lower capital gains rates on your stock's appreciation.

There's one crucial catch - you must take all your company stock out at once as part of a complete distribution or rollover of your retirement account. This isn't a strategy you can use piecemeal; it's an all-or-nothing decision that requires careful planning.

Let's break down how NUA taxation works:

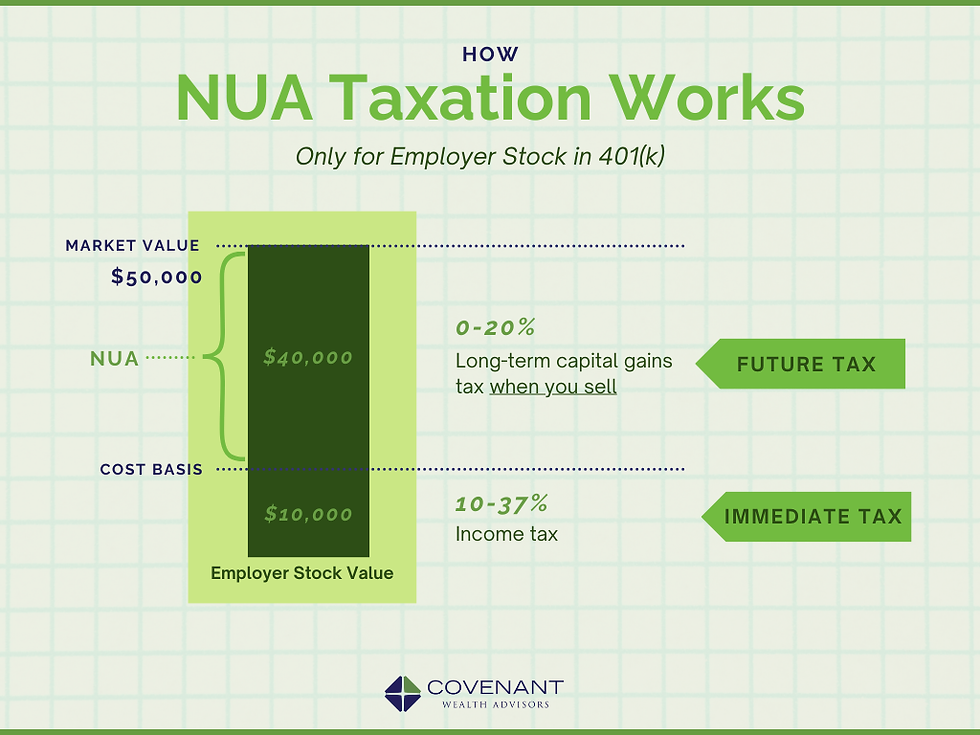

When you move your company stock from your retirement plan to a brokerage account, you'll pay taxes in two stages:

Immediate Tax: You'll pay ordinary income tax (your regular tax bracket) on what you originally paid for the stock (the cost basis).

Future Tax: When you eventually sell the stock, you'll pay the lower long-term capital gains rate (typically 15-20%) on all the appreciation that occurred while the stock was in your retirement account.

For example, if you paid $10,000 for stock now worth $50,000:

You'll pay ordinary income tax on the $10,000 basis immediately

You'll pay long-term capital gains tax on the $40,000 appreciation when you sell

Important Considerations:

You must take all your retirement account assets out at once to qualify for NUA treatment

If you don't follow the NUA rules exactly, all gains will be taxed at your higher ordinary income rate

If you're under 59½, you may face a 10% early withdrawal penalty on the cost basis

State taxes may also apply, depending on where you live

Given the complexity of NUA rules and their significant tax implications, many investors work with a financial advisor to:

Determine if NUA makes sense for their situation

Time the distribution properly

Understand potential penalties and exemptions

Evaluate alternatives like IRA rollovers

This decision requires careful analysis of your personal tax situation, retirement goals, and overall financial plan. For the most current rules and requirements, refer to IRS Publication 575 or request a free retirement assessment from Covenant Wealth Advisors.

Navigating NUA: Strategies and Considerations

Investors use several approaches based on factors like income, potential gains, and available tax treatments for retirement savings plans and their distribution options including any Rollover IRA considerations.

Here’s a breakdown of common methods:

Rollover to IRA

The simplest option is moving your company stock into a traditional IRA. While this keeps everything tax-deferred for now, you might pay more in taxes later.

Here's why:

Pros:

No immediate taxes due

Continues tax-deferred growth

Simplifies your retirement accounts

Cons:

Loses the special NUA tax break

All future withdrawals taxed as ordinary income (potentially 37%)

10% early withdrawal penalty if you take money out before age 59½

Think of it like trading a tax discount tomorrow for convenience today. While rolling over to an IRA is straightforward, it means giving up the chance to pay lower capital gains rates (typically 15-20%) on your stock's appreciation.

2. Lump-Sum Cash Out with NUA Election

This strategy involves taking all your company stock out of your retirement plan at once and selling it for cash.

While potentially powerful, timing and execution are critical.

How it Works:

Take a complete distribution of your company stock

Sell the stock for cash

Pay taxes in two stages:

Now: Ordinary income tax on what you originally paid for the stock

Later: Lower capital gains tax on the stock's appreciation when sold

Key Benefits:

Potentially lower overall taxes through capital gains rates

Immediate access to funds

Flexibility to reinvest as you choose

Important Cautions:

Must distribute ALL retirement plan assets at once to qualify

Triggers immediate tax bill on your cost basis

10% early withdrawal penalty if under age 59½

You have just 60 days to decide whether to reinvest in an IRA

Missing deadlines or steps could disqualify NUA treatment

For example: If you paid $10,000 for stock now worth $50,000:

Pay ordinary income tax now on $10,000

Pay lower capital gains tax on $40,000 when you sell

Add 10% penalty on $10,000 if under 59½

3. Lump-Sum In-Kind Distribution to Brokerage Account with NUA Election

In our opinion, the most flexible NUA strategy involves moving your company stock directly to a regular brokerage account while keeping the shares intact.

This approach gives you control over when to sell while preserving the tax advantages of NUA.

How It Works:

Instead of selling your shares immediately, you transfer them "in-kind" to a regular brokerage account. This means you keep the actual shares rather than converting them to cash.

You'll need to take all your retirement plan assets out at once to qualify for NUA treatment, but you can then hold the stock as long as you wish.

The Tax Timeline:

When you transfer: Pay ordinary income tax on your original purchase price

When you eventually sell: Pay lower capital gains rates on the stock's appreciation

Any additional gains after transfer: Taxed based on how long you hold the shares

Key Benefits:

Maximum control over timing of stock sales

Potential to capture additional market gains

Flexibility to sell shares gradually over time

Opportunity for tax-loss harvesting with other investments

Important Considerations:

Must distribute your entire retirement plan balance at once

Immediate tax bill on the cost basis

10% early withdrawal penalty if under 59½

Concentrated position risk from holding single-stock

May face state taxes depending on your location

This strategy works best for those who:

Believe in their company's long-term prospects

Can afford to pay the immediate taxes

Want to maintain control over their investment timing

Are comfortable managing a brokerage account

FAQs about Net Unrealized Appreciation

What does net unrealized appreciation mean?

Net unrealized appreciation (NUA) is the difference between the cost basis of company stock in a retirement plan and its market value when distributed.

How does NUA work in a 401k?

When taking a lump-sum distribution of company stock from a 401(k), you can elect NUA treatment. This taxes the NUA at long-term capital gains rates upon sale, not as ordinary income.

The cost basis is still taxed as ordinary income at distribution.

How to report net unrealized appreciation?

NUA is reported on IRS Form 1099-R. Box 1 on this form will show the gross amount distributed from the retirement plan, with the taxable amount of this distribution shown in Box 2a. The NUA amount (the cost basis), which is essentially the difference between Box 1 and Box 2a, is reported in Box 6.

The NUA is generally taxed when the stock is sold according to rules pertaining to such income/gains. IRS Publication 575 provides details on reporting this amount.

What are the disadvantages of a NUA?

NUA requires a lump-sum distribution, meaning you withdraw all employer stock at once. The cost basis is taxed as ordinary income immediately. You'll also assume more market risk by holding a concentrated stock position and may forfeit the account protection afforded within a qualified retirement plan.

See How Our Financial Advisors Can Help You Retire With Confidence

Retirement Planning - Optimize your income and create a roadmap for a secure retirement.

Investment Management - Personalized investing to grow and protect your wealth.

Tax Planning - Identify tax strategies including Roth conversions, RMD management, charitable giving and more...

Conclusion

NUA provides a valuable opportunity for managing your wealth tax-efficiently during retirement. You can maximize this tool by learning how NUA works, exploring different strategies, and consulting with a financial advisor.

By including NUA in a well-defined financial plan, you gain more control over your retirement assets, minimize your tax burden within the bounds of any current laws that may apply during such year the income is received or any gains recognized and assets sold or amounts equal to gains withdrawn, ultimately improving your after-tax income in retirement. Consider the implications of a traditional IRA and Roth IRA as those have different income tax and gain tax treatments under relevant IRS publications that could apply depending on each person's specific needs for asset distributions and any tax planning and wealth management.

Do you want to retire without running out of money? Request a free retirement assessment today!

About the author:

Senior Financial Advisor

Scott is a Financial Advisor for Covenant Wealth Advisors, a CERTIFIED FINANCIAL PLANNER™ practitioner and a Certified Public Accountant (CPA). He has over 17 years of experience in the financial services industry in the areas of financial planning, tax planning, and investment management.

Disclosures: Covenant Wealth Advisors is a registered investment advisor with offices in Richmond, Reston, and Williamsburg, VA. Registration of an investment advisor does not imply a certain level of skill or training. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. The views and opinions expressed in this content are as of the date of the posting, are subject to change based on market and other conditions. This content contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Please note that nothing in this content should be construed as an offer to sell or the solicitation of an offer to purchase an interest in any security or separate account. Nothing is intended to be, and you should not consider anything to be, investment, accounting, tax, or legal advice. If you would like accounting, tax, or legal advice, you should consult with your own accountants or attorneys regarding your individual circumstances and needs. This article was written and edited by a CERTIFIED FINANCIAL PLANNER™ professional with the assistance of AI. No advice may be rendered by Covenant Wealth Advisors unless a client service agreement is in place. Hypothetical examples are fictitious and are only used to illustrate a specific point of view. Diversification does not guarantee against risk of loss. While this guide attempts to be as comprehensive as possible but no article can cover all aspects of retirement planning. Be sure to consult an advisor for comprehensive advice.